Andrew Pyle

April 05, 2024

Having your own pension fund

In less than two weeks, the federal government will deliver its 2024 budget. Market participants will glean over its details for clues as to whether the policy framework will impact the economy, Bank of Canada rate decisions and the overall health of Canadian equity and fixed income markets vis a vis other regions. Business owners will also be interested in the economic impacts, but they will be on alert for any changes to the tax landscape. It is not lost on anyone that the last several years have seen a shift towards an increasingly tax disadvantaged environment for businesses and for how the wealth accumulated by owners faces an ever more restrictive landscape. Case in point, the recent changes to the Alternative Minimum Tax.

While it’s possible that businesses could find themselves in a more favourable setting down the road, the distance to a balanced budget makes that hard to believe. This is why small and medium-size business owners need to sharpen their pencils on how to become even more tax efficient going forward. Fortunately, there are a number of strategies available to them. One extremely powerful tool that is often overlooked, is the Individual Pension Plan, or IPP.

The Basics

First and foremost, let's grasp the fundamentals of IPPs. An Individual Pension Plan is a type of defined benefit pension plan tailored for business owners and incorporated professionals. Typically, the member of the plan would be the business owner, but it can also include a spouse or children if they are receiving salaried income from the corporation. A key individual of the company may also be a member of the plan. Now, given the way the IPP is structured, there is no meaningful difference between an RRSP and the IPP for individuals that are younger than say 37. This doesn’t mean there is no advantage of having children below that age in the IPP. They simply would be defined contribution members until they reach the age where the defined benefit advantage kicks in.

Unlike RRSPs, where there is a maximum contribution set by the CRA, IPPs calculate contribution limits based on a combination of factors including age, earnings history, and years of service. Those limits increase year by year, similar to RRSP maximums, but at a faster pace. Where an RRSP contribution is made by the business owner on after-tax salary income, an IPP contribution is made directly by the company. That contribution is tax deductible to the company. The other key difference with the RRSP is that the IPP is protected in the event that there is a judgement against you as a result of a lawsuit. For an RRSP, depending on the province you live in, it can be seized in order to meet the judgement.

Review Time

Over the life of the IPP, an actuarial review is conducted every three years. Why? Because the CRA has a prescribed rate of growth for an IPP of 7.5%, which allows for the pension benefits to be pre-defined. If the value of the IPP on its review date is less than where it should be, based on growth of 7.5% per year, then the company can make a lump-sum contribution to bring the value to that level. That contribution is also deductible for tax purposes. If the company doesn’t have the capital to make that one-time contribution, it can amortize it over a number of years.

An RRSP has no such rule. It can go up and it can go down, but the government doesn’t allow you to add more money if it hasn’t grown at a certain pace. For companies that have accumulated a significant amount of retained earnings – perhaps to the extent that passive investment income now exceeds the new threshold of $50,000 – this ability to deduct contributions results in enhanced tax efficiency. If, on the other hand, the value of the IPP on its review date is higher than where it should be, the company can continue to make annual contributions, provided it doesn’t become an excessive surplus.

Creating the IPP

Several factors go into the setting up the IPP, including the age of the owner or member, salary and something called past service. This refers to an amount that would need to go into an IPP to bring it to the same value as if the individual had started the IPP at the inception of the company. Salary information dating back to that date is then used, alongside the 7.5% prescribed growth and assumed inflation of 4%, which is also prescribed by CRA.

The longer the corporation has been in existence, with the owner or member drawing a salary, the larger the past service amount will be, all other things being equal. Whatever that past service amount is, it will be made up by a required contribution of RRSP assets and a lump-sum cash contribution by the corporation. Each year after inception, the annual contribution will be determined by salary and age, again with a review taking place every three years.

Comparing IPP and RRSP Accumulation

To get a sense for how superior the IPP is versus the RRSP, I have put together two hypothetical examples – one for a 40yr business owner and the other for someone who is 55. In both cases, we assume that the owner/individual started working in their early 20s and that the corporation was created at the same time. These examples were generated by Buck Canada HR Services. These examples are illustrations only, but I have shown the comparative assumptions below:

Assumptions 40yr old 55yr old

Date of birth Jan 1, 1984 Jan 1, 1969

Date of hire Jan 1, 2004 Jan 1, 1991

Starting salary $150,000 $125,000

Past service date Jan 1, 2004 Jan 1, 1991

Effective date of IPP Jan 1, 2024 Jan 1, 2024

Current salary $200,000 $200,000

RRSP assets available $650,000 $950,000

Fund growth rate 7.5% 7.5%

Salary increase rate 5.5% 5.5%

Inflation rate 4.0% 4.0%

Retirement age 65 65

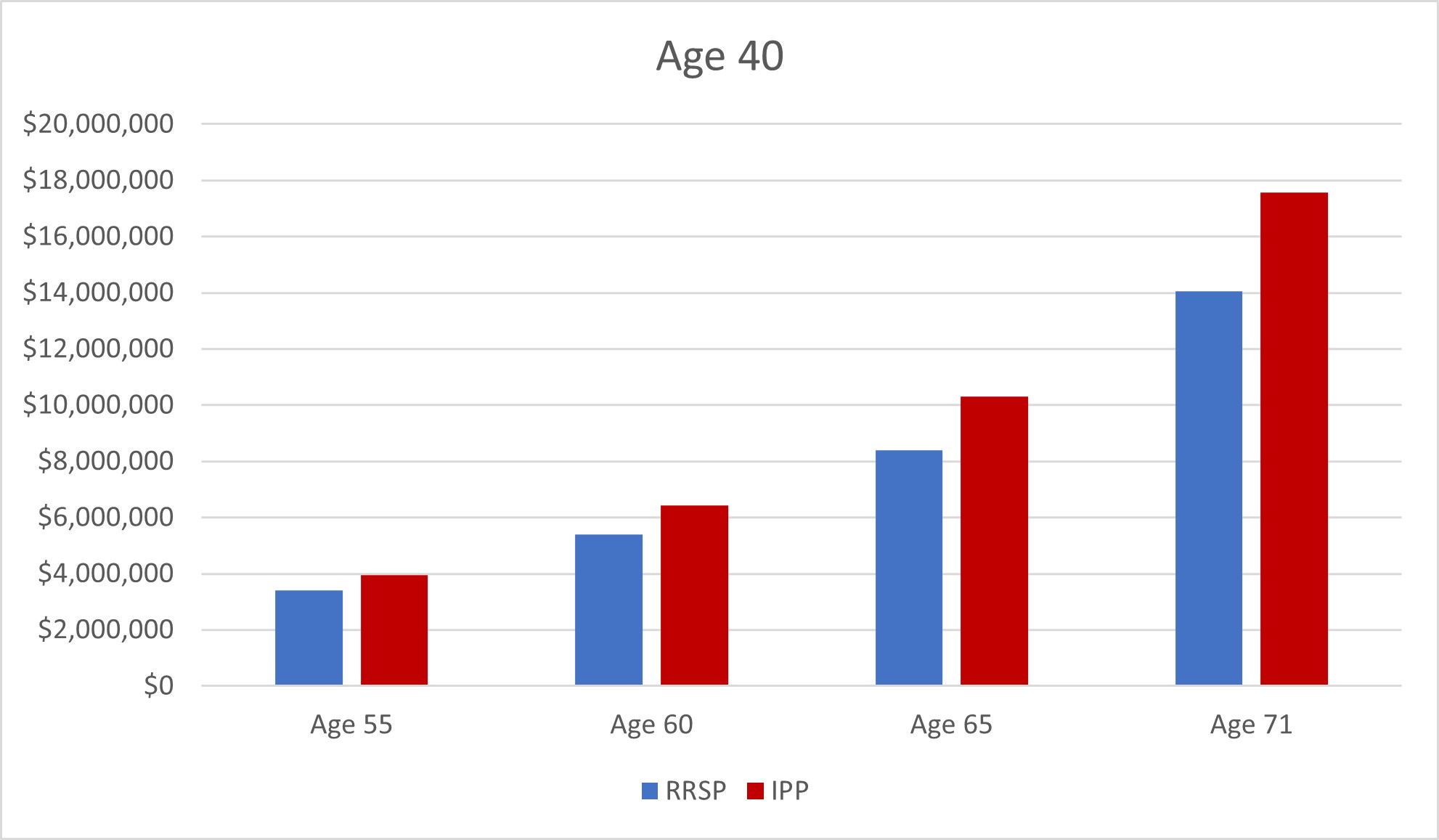

The following chart shows how the 40yr old fares in accumulating funds in an RRSP versus an IPP. By age 55, there is already roughly a $500,000 outperformance by the IPP, but that grows to close to $1 million by age 60 and around $3 million by 71.

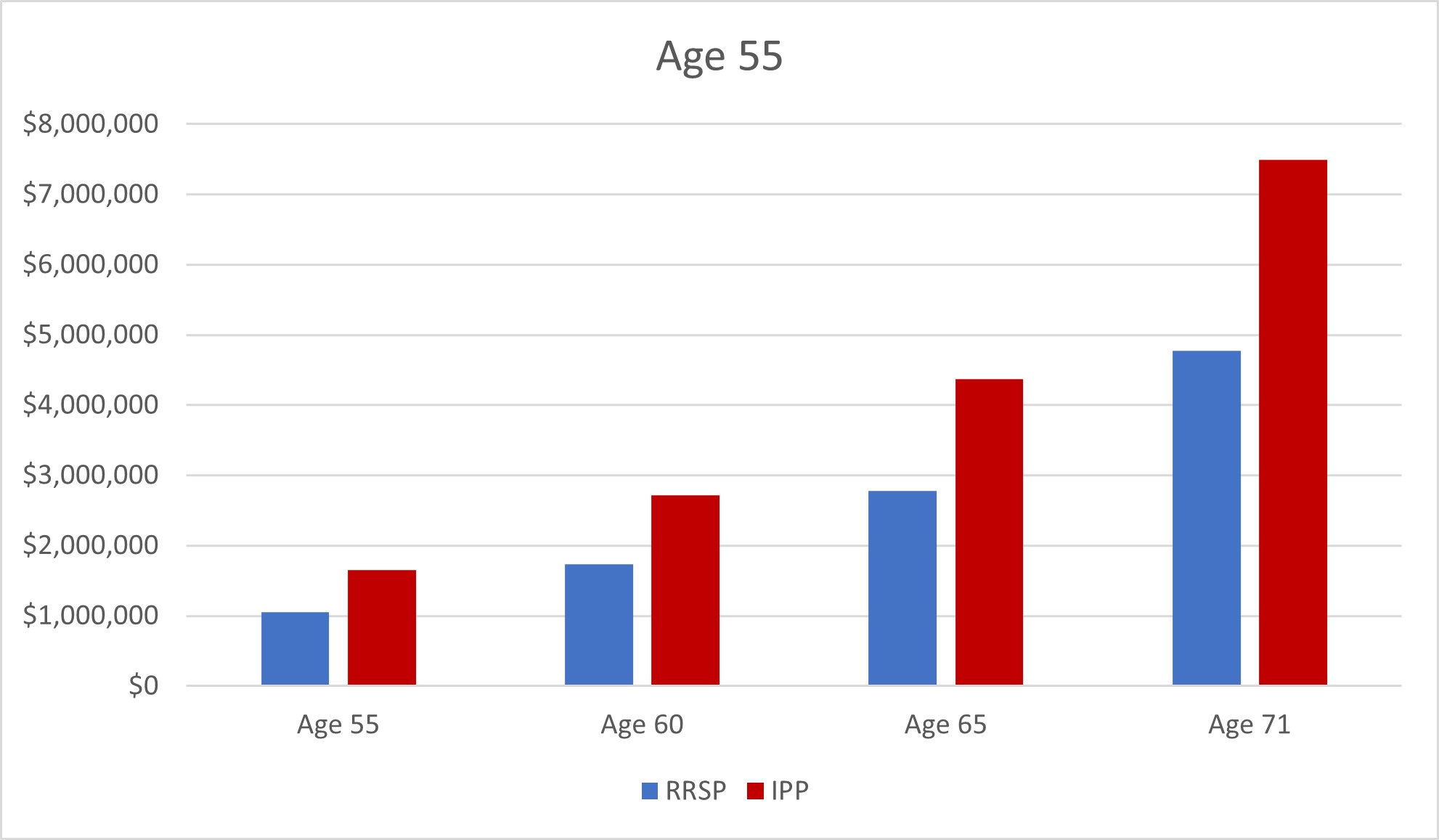

The next chart shows the same comparison for the 55yr old in an RRSP versus an IPP. Even though the individual is already 55, in that year the IPP is approximately $600,000 more than what the RRSP was, as a result of the past-service top-up. By age 60, the difference is close to $1 million and in five more years the outperformance is around $1.9 million. You may wonder why these gaps are still significant even though the individual is starting the IPP later in their career? The answer is that the contribution amounts become so large relative to the maximum RRSP contributions that there is still a sizable advantage.

Retirement time!

Similar to the RRSP, you have options when it comes down to what to do with the IPP at retirement. You can retire starting at age 55 and begin receiving income. For an RRSP, this means converting to a RRIF or buying an annuity. Either has to happen by the end of the year you turn 71. For an IPP, you can elect to start receiving pension income from age 55 on. The difference is that while receiving pension payments, the corporation may be allowed to keep contributing in order to ensure that the payments can be maintained.

The most common practice, however, is to wind up the IPP before or in the year you turn 71. The reason why has to do with flexibility of capital, but mainly what happens at death. For an IPP, the surviving spouse is entitled to two-thirds of the pension payments. In winding up the IPP, a maximum amount can be transferred into a locked-in registered retirement account, determined by the CRA. If the individual had transferred in RRSP assets on a voluntary basis, these come back out into either an RRSP or RRIF. The remainder is paid out in the form of cash, which is taxable. If the individual passes, then the retirement accounts would transfer to the surviving spouse on a tax deferred basis and that spouse would receive 100% of the pension flow from those accounts.

Other benefits

Which leads us to another advantage. While an individual is required to transfer in a specific amount of RRSP assets as part of past service, they can also transfer in RRSP assets on a voluntary basis. Why would you do this? Well, if you are paying an investment management fee on your RRSP, that fee cannot be deducted for tax purposes. Fees paid for managing an IPP, however, are deducted by the corporation, just like administrative and actuarial fees. Moving non-deductible RRSP fee-based assets into the IPP provides even more tax efficiency for the corporation.

We have been working with business owners from various sectors, including healthcare, on how IPPs can be incorporated into the overall wealth plan. While tax legislation will always change and not necessarily to the benefit of businesses, creating a pension plan within the company is an effective way to enhance wealth accumulation, increase tax efficiency and even augment estate planning. The hypothetical illustrations shown above can be done on a customized basis and performed in the context of a financial plan to see whether there is an advantage or not.

On behalf of the Pyle Wealth Advisory team, have a wonderful weekend.

Andrew Pyle

CIBC Private Wealth consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc. Insurance services are available through CIBC Wood Gundy Financial Services Inc. In Quebec, insurance services are available through CIBC Wood Gundy Financial Services (Quebec) Inc. The CIBC logo and “CIBC Private Wealth” are trademarks of CIBC, used under license. “Wood Gundy” is a registered trademark of CIBC World Markets Inc.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2024.

Given the complexities involved, specialized tax and pension advice must be sought to ensure an Individual Pension Plan (IPP) is appropriate to individual situations. An IPP strategy must be considered within the context of a comprehensive financial and estate plan.

Andrew Pyle is an Investment Advisor with CIBC Wood Gundy in Peterborough. Andrew and his clients may own securities mentioned in this column. The views of Andrew Pyle do not necessarily reflect those of CIBC World Markets Inc.

These calculations and projections are for demonstration purposes only. They are based on several assumptions and consequently actual results may differ, possibly to a material degree.

If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.

Clients are advised to seek advice regarding their particular circumstances from their personal tax and legal advisors.

Related posts

Andrew Pyle

May 03, 2024

Canada versus U.S. positioning

The Canadian economy looks to be on a weaker trajectory than south of the border, which will make it hard for Canadian stocks to close the gap with the U.S.

Read moreAndrew Pyle

May 02, 2024

BNN Bloomberg - The Street

Andrew Pyle joins BNN Bloomberg, to discuss the Fed's rate cut expectations.

Read more